The Internal Audit Department activities are carried out by the Code of Ethics and International Standards for the Professional Implementation of Internal Control.

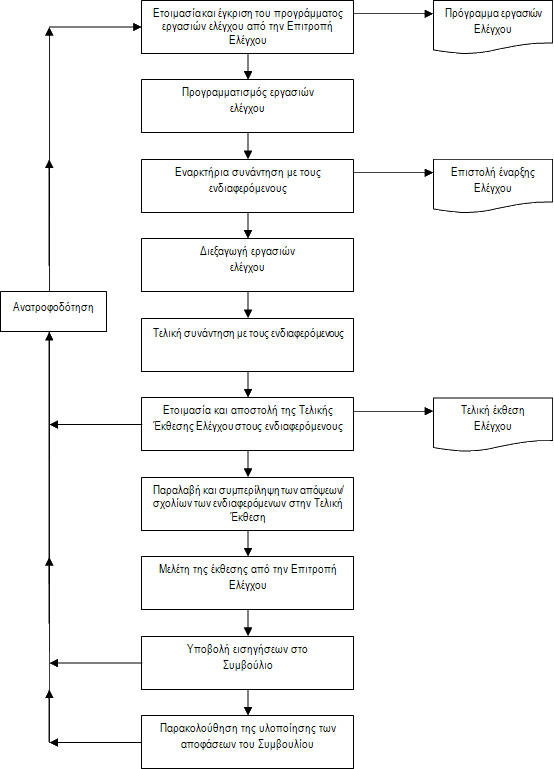

Preparation and Approval of Audit Work Programme:

The Internal Audit Department establishes an one-year, two-year or three-year audit work, based on an appropriate risk assessment methodology, including any risks or concerns identified by the Senior Management / Executive Bodies of the University or the Audit Committee. The Audit Work Plan is submitted for approval to the Audit Committee at the beginning of the year and reviewed at any stage during the year, if deemed necessary.

Control stages:

Opening meeting

The control operations begin with an opening meeting for discussion between Officers / Assistant Officers of the Internal Audit Department and Officers of the controlled Department / Service, on the control’s aim and target. It is noted that the control work may start without notice or meeting, if judged that sudden control better ensures the success of the audit objectives.

Control operations conduct

Since each test is unique, the control conducting procedures may vary. In a typical test, the Officers of the Internal Audit Department assess the effectiveness of internal control systems, designed and adopted in a Department / Service and control the compatibility of the procedures applied by these systems.

Final meeting with interested parties

Upon completion of control tasks all questions/issues to be updated and/or further clarified by interested parties are marked.

In the final clarification meeting with the interested officers of Services / Departments, a presentation of themes / issues, findings and recommendations is carried out, and final opinions and recommendations are determined.

Preparation and delivery of the Audit Report to the interested parties

The Internal Auditor shall forward his final Report to the interested parties for any comments / opinions/suggestions.

The final Audit Report comprises of the following:

- Executive summary of the main conclusions and recommendations.

- Detailed Report with observations, findings, conclusions and recommendations.

- Any other information / reports / documents deemed necessary.

Report study by interested parties and submission of comments / opinions /

recommendations

The interested parties shall submit to the Internal Auditor comments / views / recommendations within 10 working days from the date of the final report dispatch. In case of no reply within the above timeframe shall imply that the above-mentioned parties do not have any comments / opinions or suggestions and that they agree with the content, conclusions and recommendations of the Report.

Final Report of the Internal Auditor, together with the views / comments / suggestions of interested parties, are submitted to the Audit Committee for study and submission of recommendations to the Council.

It is noted that the internal auditor's report are not discussed in another Body / Committee before being studied by the Audit Committee.

Study Report of the Audit Committee:

The Audit Committee studies the Audit Report and the comments / views of interested parties.

Submitting Suggestions

The Audit Committee submits its suggestions to the University Council for decision making.

Decision Making Follow Up:

The Internal Audit Department monitors the implementation of decisions by the Council of the University and informs the Audit Committee accordingly.

Feedback

The results of the audit, the Audit Committee’s decisions and their implementation by the competent Services are used for the preparation of the audit plan for the following year.

Procedures Workflow